Though Pittsburgh’s Industrial real estate market remained stable throughout 2023, there are indicators that 2024 could bring some slight softening in vacancies, rents, and investment levels. While a cooling at the national level will impact demand in Pittsburgh, its effects are unlikely to be significant. Because Pittsburgh is not a distribution hub, construction has always been constrained and there is little risk of over-saturation. The market’s net absorption of industrial space was a robust 1.7 million SF in 2023, and local vacancies hovered around 5.5% throughout the entirety of the year.

Fourth quarter 2023 closed with a direct vacancy rate of 3.73%, an overall vacancy rate of 4.05%, and an average asking direct rental rate reported at $7.75 per sq. ft. NNN. In December, the Michigan unemployment rate was recorded at 4.3%, identical compared to this time last year. The US job market continues to remain resilient despite an uncertain economy and elevated interest rates. In October, employers posted 8.9 million jobs tumbling to the lowest level since March 2021, while in December openings slightly increased with employers posting 9 million jobs, compared to 8.8 million in November. Recent data indicates a gradual movement towards a balanced pre-pandemic job market with hiring remaining steady and limited number of layoffs. University of Michigan economists are projecting a full recovery of jobs for Michigan by early 2024, followed by two years of growth and a decline in terms of inflation. US consumer inflation eased slightly in November, while consumer confidence to some degree increased during December. The Michigan economy holds steady despite facing several challenges throughout the year including an automotive strike, supply chain shortages, and elevated interest rates bearing an impact on loans and US home sales. The Federal Reserve closed out 2023 with the decision to keep the key interest rate unchanged since the last increase of 0.25% in July and appear to be confident in a “soft landing” of the economy in 2024.

Fourth quarter 2023 closed with a direct vacancy rate of 21.54%, an overall vacancy rate of 24.22%, and an average asking direct rental rate reported at $19.02 per sq. ft. In December, the Michigan unemployment rate was recorded at 4.3%, identical compared to this time last year. The US job market continues to remain resilient despite an uncertain economy and elevated interest rates. In October, employers posted 8.9 million jobs tumbling to the lowest level since March 2021, while in December openings slightly increased with employers posting 9 million jobs, compared to 8.8 million in November. Recent data indicates a gradual movement towards a balanced pre-pandemic job market with hiring remaining steady and limited number of layoffs. University of Michigan economists are projecting a full recovery of jobs for Michigan by early 2024, followed by two years of growth and a decline in terms of inflation. US consumer inflation eased slightly in November, while consumer confidence to some degree increased during December. The Michigan economy holds steady despite facing several challenges throughout the year including an automotive strike, supply chain shortages, and elevated interest rates bearing an impact on loans and US home sales. The Federal Reserve closed out 2023 with the decision to keep the key interest rate unchanged since the last increase of 0.25% in July and appear to be confident in a “soft landing” of the economy in 2024.

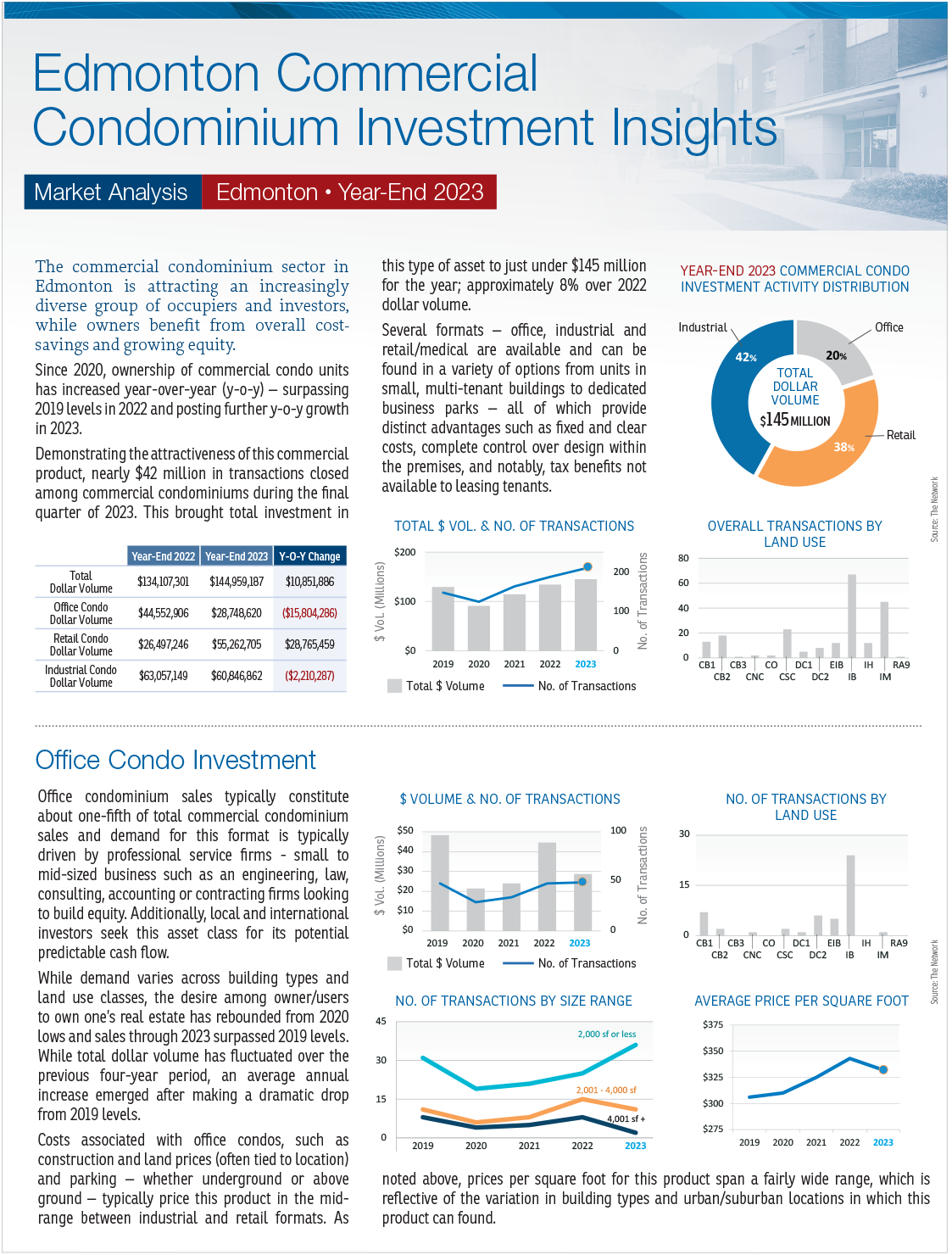

The commercial condominium sector in Edmonton is attracting an increasingly diverse group of occupiers and investors, while owners benefit from overall cost-savings and growing equity. Since 2020, ownership of commercial condo units has increased year-over-year (y-o-y) – surpassing 2019 levels in 2022 and posting further y-o-y growth in 2023.

In recent years, ownership of commercial condo units has increased significantly in the Calgary market. Several formats – office, industrial and retail/ medical are available and can be found in a variety of options from units in small, multi-tenant buildings to dedicated business parks – all of which provide distinct advantages such as fixed and clear costs, complete control over design within the premises, and notably, tax benefits not available to leasing tenants.

“Investors came back to Edmonton’s commercial real estate (CRE) investment market and liked what they saw in 2018. Total dollar volume invested exceeded $2.65 billion, driven by renewed interest in ICI Land, plus strong demand for Multi-Residential properties.”

“Investors are back and active in Edmonton’s commercial real estate (CRE) investment market in a meaningful way. Led by a resurgence of interest in ICI Land and an uptick in demand for Multi-Residential properties and Industrial assets, total dollar volume invested rose by 8% year-over-year.” -- Doug Grinde, Vice President, Barclay Street Real Estate

“Investors are back in Calgary’s commercial real estate (CRE) investment market and their wallets are open. Fuelled by a continued desire for retail assets and renewed interest in ICI and Residential Land, total dollar volume invested rose by 23% year-over- year.” -- George Larson, Vice President, Investment Sales, Barclay Street Real Estate

AT THE MID-POINT OF 2018, CALGARY’S RETAIL MARKET CONTINUED TO GRAPPLE WITH A FLOOD OF VACANT SEARS RETAIL SPACE THROUGHOUT THE CITY.

At the end of the first quarter of 2018, the industrial market of the Mexico City Metropolitan Area recorded an inventory of 9.6M SQM or 103.7M SQFT of Class A warehouses, concentrated mainly in the Cuautitlan 30%, Toluca 19%, and Tultitlan 17% submarkets.

TCN Worldwide's State of the Market: Eastern Edition, 4th Quarter 2015 Prepared by Hugh F. Kelly, PhD, CRE, Consulting Economist to TCNIn this edition: –Overview of National Economic Context –Regional Conditions in the Eastern States –Commercial Property Investment Trends

TCN Worldwide's State of the Market: Eastern Edition, 3rd Quarter 2015 Prepared by Hugh F. Kelly, PhD, CRE Consulting Economist to TCNIn this edition: –Overview of National Economic Context –Regional Conditions in the Eastern States –Commercial Property Investment Trends

"As we enter the second half of 2015 we see markets which are continuing to trend towards favorable levels. Buyers are beginning to respond to the Federal Reserve’s hint of an interest rate increase later this September. We see a pronounced increase in the acquisition market and anticipate this activity will continue going forward into 2016."

"Second quarter 2015 continues an ongoing positive trend ... our seventeenth straight quarter of positive absorption."

Research and analysis by Hugh Kelly

"2021 will be the year of retail recovery, but it will be a very uneven, choppy recovery."

"2020 is a year that will long be remembered as one of significant upheaval and uncertainty and the Oklahoma City office market was certainly not immune to that."

According to the U.S. Census Bureau, retail sales during May 2020 were up 17.7% seasonally adjusted from the prior month but down 6.1% year-over-year. That follows a record-setting 14.7% drop in April 2020 (month-over-month).

The last 12 months have been marked by dramatic changes. As of this writing, these events have not seriously affected the Oklahoma City multi-tenant industrial market. Overall, multi-tenant industrial properties have continued the declining vacancy trend seen over the past two years. The bulkwarehouse sector is the exception this year.

During the first half of 2020 the market vacancy rate rose from 20.9% to 23.5% in the first half of 2020. The rise in vacancies has been market-wide with the Central Business District vacancy rate rising from 21.8% to 23.6% and the suburban submarkets rising from 20.8% to 23.4% vacant. Market-wide rental rates showed a slight dip from $19.53 per square foot to $19.45 per square foot. The market experienced negative absorption of nearly 536,000 square feet which was market-wide in nature rather than limited to one or two submarkets. The CBD experienced negative absorption of 146,000 SF and the suburban submarkets totaled nearly 390,000 SF of negative absorption.

TCN Worldwide's State of the Market: Western Edition, 2nd Quarter 2016 Prepared by Hugh F. Kelly, PhD, CRE, Consulting Economist to TCN WorldwideIn this edition: –National and Macroeconomic Overview –Regional Conditions in the Western States –Commercial Property Investment Trends

As we enter the fifth year of the latest "tech boom," there are some pretty compelling signs that the "party is almost over."

TCN Worldwide's State of the Market: Western Edition, 1st Quarter 2016 Prepared by Hugh F. Kelly, PhD, CRE, Consulting Economist to TCNIn this edition: –Overview of National Economic Context –Regional Conditions in the Western States –Commercial Property Investment Trends

Stark & Associates Retail Market Newsletter for the Northern Nevada Market. Local experts are bullish on Nevada...

TCN Worldwide's State of the Market: Western Edition, 3rd Quarter 2015 Prepared by Hugh F. Kelly, PhD, CRE Consulting Economist to TCNIn this edition: –Overview of National Economic Context –Regional Conditions in the Western States –Commercial Property Investment Trends

{kind=link}