In the first half of 2024, vacancy rates held steady at 24%. Rental rates were also unchanged from year-end 2023, sitting at $27 per square foot. Absorption trends were notably poor with negative 814,000 square feet absorbed so far this year. This is more than double the negative 411,000 square feet absorbed through the entirety of 2023.

In Q2/24, the downtown office market’s vacancy rate surpassed 22%, an increase from 20% at year-end 2023. Absorption improved, but remained negative at -67,000 square feet in Q2, bringing the year-to-date number to negative 1.9 million square feet, more than double the negative net absorption over the same period last year. Despite these weak headline statistics, there are pockets of strength in the CBD. For example, Fulton Market continues to outperform, posting positive absorption every year since 2016.

The recovery of Calgary’s Downtown office market held strong during the second quarter of 2024. Overall availability – and particularly the vacant component – of Downtown office space posted another quarter-over-quarter decrease as we closed the first half of 2024. Just under 208,000 square feet of headlease space was taken through the second quarter, bringing the vacancy rate down even further. We also saw an uptick in new space marketed for sublease, sub-sublease and/or office share, which caused the overall availability rate for the Downtown to increase slightly.

Overall availability – and particularly the vacant component – of Calgary’s suburban office market was remarkably stable during the second quarter of 2024. The availability rate increased just slightly on approximately 21,000 square feet of negative absorption, which was due in large part to some larger spaces being marketed for sublease.

Calgary’s overall retail availability rate increased further during the second quarter of 2024, reaching 4.6%. As stated in our previous edition of this report, the level of available space on the market at June 30th has Calgary approaching what we consider to be a balanced market in which the variety of options for would-be tenants and existing tenants alike and allows for rental rates to stabilize among the various sizes, formats and locations of options on the market. Despite a slight-yet-ongoing increase in available space being marketed, the situation remains remarkably stable given the substantial increase in Calgary’s retail inventory since early 2015; currently 44.8 million square feet (msf) versus 37.2 million msf at mid-year 2015 when multiple store chains began shutting their doors via major closures and consolidations.

Calgary’s Downtown office market is indeed getting healthier. Overall availability – and particularly the vacant component – of Downtown office space posted another quarter-over-quarter decrease as we moved into 2024. Just under 211,000 square feet of space was taken, which includes South Bow Corporation taking approximately 87,000 square feet pf space in 707 5th and National Bank of Canada taking approximately 44,000 square feet pf space in Banker’s Court. As of March 31st, there were just under 1,077 spaces throughout the Downtown being marketed for immediate occupancy. The last time there were this few listings was the 4th quarter of 2017 when, coincidentally, Downtown inventory was similar to present as it was prior to the completion of TELUS Sky.

Calgary’s overall retail availability rate increased during the first quarter of 2024, reaching 4.3%. This level of available space has Calgary approaching what we consider to be a balanced market; there is a variety of options for would-be tenants and existing tenants alike which is allowing rental rates to stabilize after several quarters of increases. Calgary experienced overall availability in this 4.5%–5.5% range in the not-too-distant past, when the closure of Sears Canada put 650,000 square feet of retail space on the market in Q1 2018. Availability increased to 5.1% in that quarter but by year-end, overall availably had dropped to 4.6% and remained in the low-to-mid 4% range through 2019.

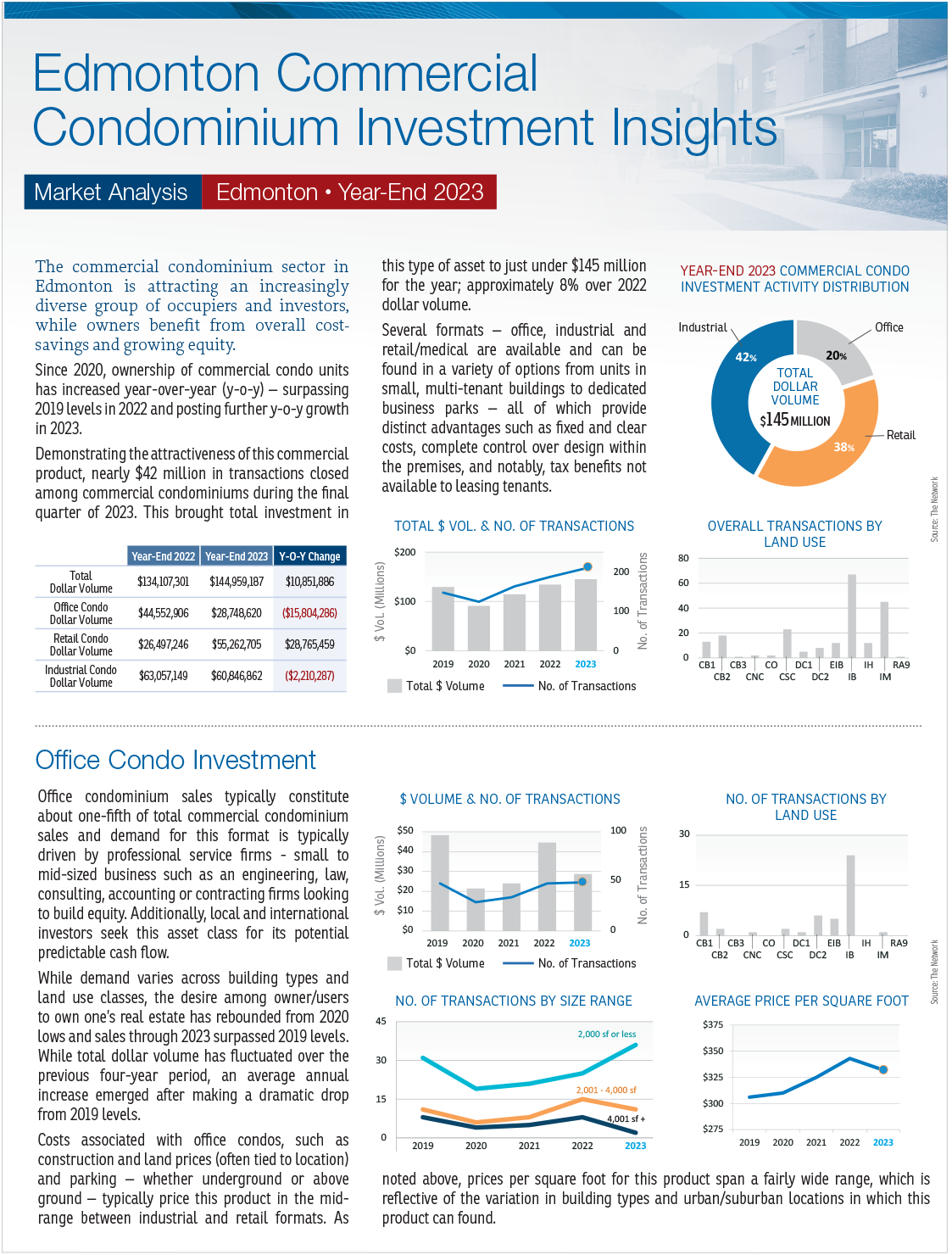

The commercial condominium sector in Edmonton is attracting an increasingly diverse group of occupiers and investors, while owners benefit from overall cost-savings and growing equity. Since 2020, ownership of commercial condo units has increased year-over-year (y-o-y) – surpassing 2019 levels in 2022 and posting further y-o-y growth in 2023.

In recent years, ownership of commercial condo units has increased significantly in the Calgary market. Several formats – office, industrial and retail/ medical are available and can be found in a variety of options from units in small, multi-tenant buildings to dedicated business parks – all of which provide distinct advantages such as fixed and clear costs, complete control over design within the premises, and notably, tax benefits not available to leasing tenants.

Availability in Calgary’s Beltline office market increased ever-so-slightly during the final quarter of 2023. A spike in sublease availability resulted in approximately 20,000 square feet (sf) of negative net absorption. The new space introduced to the market was primarily available for sublease and located in polar opposites of the size spectrum: pockets measuring 2,000 – 4,000 sf and in large 10,000+ sf spaces. With such a small net change in overall occupied space, total occupied space in the Beltline remained largely consistent with the previous quarter at 75.7%.

TCN Worldwide's State of the Market: Eastern Edition, 3rd Quarter 2017 Prepared by Hugh F. Kelly, PhD, CRE, Consulting Economist to TCN Worldwide. In this edition: –National and Macroeconomic Overview –Regional Economic Conditions –Commercial Property Investment Trends

The Manhattan office leasing market ended the third quarter with more than 9 million square feet newly leased. The average rental price was $65.70, an increase from Q2. Of note, Landlord incentives provided to Tenants have also expanded and increased.

Absorption totaled 18,745 sq. ft. in the Second Quarter 2017. Solid figures considering the run this market has enjoyed over the past several quarters.

TCN Worldwide's State of the Market: Eastern Edition, 2nd Quarter 2017 Prepared by Hugh F. Kelly, PhD, CRE, Consulting Economist to TCN Worldwide. In this edition: –National and Macroeconomic Overview –Regional Economic Conditions –Commercial Property Investment Trends

The Manhattan office leasing market ended the second quarter of 2017 with a negative absorption of nearly 630,000 square feet, more than 1,000,000 square feet stronger than Q1. The vacancy rate citywide is now 8.2% having ticked downwards by 0.2% almost 1.5% stronger than the national marketplace. Average rents across the Manhattan office market fell to just below $60psf. The pricing correction and significantly lower negative absorption rate indicates a leveling of the office leasing market.

A number of leases were signed during the fourth quarter. First in Livonia, Cabinetworks Group, LLC inked a deal totaling 89,543 sq. ft. of Class B office space located at 20000 Victor Parkway. In Bingham Farms, Hondros College of Nursing signed a deal for 48,035 sq. ft. of Class B office space located at 30700 Telegraph Road in the Bingham Office Center. Lastly, in Ann Arbor, Tetra Tech, Inc., a global provider of consulting and engineering services leased 21,890 sq. ft. located at 1136-1138 Oak Valley Drive in the Valley Ranch Business Park.

Fourth quarter 2022 closed with a direct vacancy rate of 3.74%, an overall vacancy rate of 4.24%, and an average asking direct rental rate reported at $7.20 psf. In December, the Michigan unemployment rate was recorded at 4.3%, a decrease of 1.3 percentage points compared to this time last year, while the U. S. unemployment rate was recorded at 3.5%. Despite the Federal Reserve’s intentions to slow the demand for labor, wage gains and inflation with their continued interest rate hikes, the number of U.S. job openings in December was recorded at 11M, up from 10.46M in November as employers continued hiring at a solid pace. During fourth quarter, the U.S. economy grew by 2.9% and 2.1% throughout 2022, recording six straight months of stable growth. In December, indicators pointed towards the easing of inflation as consumer spending decreased by 0.2% from November along with a decline in consumer prices. It is expected the Federal Reserve will raise the key interest rate during 2023, with the number of increases to be determined. As inflation reached a 40-year high, seven interest rate increases were recorded during 2022 with the final increase of the year by half a point reaching the highest level in 15 years. Inflation remains one of the top economic concerns as consumers remain cautious, re-evaluate their spending habits and outlook towards saving and borrowing.

SUPPLY, MEET DEMAND. Multi-Tenant property has had its hay-day since first dropping N of 45% of vacancy from 2020-2021 (14.93% vacancy to 8.38%). With the vacancy rate bottoming out at a record shattering figure of 4.64% in 2022, it appears we may be headed towards stabilization. As any reasonable investor should expect, this sub-sect of the Industrial Market has seen its fair share of renovation and a large amount of spec construction. This race to meet the demand in tandem with a questionable political and economic outlook for the Country has been met with a marginal raise in vacancy to 5.42%. While this figure doesn’t swing the needle to indicate a over-supply in the market, it isn’t something to ignore either. With the Medical Cannabis industry tightening regulations and interest rates rising, this percentage may continue to creep up for a time. Regardless, this market is showing resilience and we believe it will continue to do so.

The multi-family market, more than any other, has been driven by the money funneled into the economy during the course of the pandemic. The shear level of money provided to renters through various pandemic programs combined with the broader economic stimulation led to some of the largest multi-family rent increases in our history. Oklahoma City has historically seen slow but steady rent growth; two to three percent annually. You could always count on it. In 2021, rent increased 12 percent. The increase was cut in half but still historically high in 2022, at 6 percent, with most of this moderation coming in the second half of the year. Clearly this wasn’t sustainable. What isn’t clear is where do we go from here.

Third quarter 2022 closed with a direct vacancy rate of 20.71%, an overall vacancy rate of 22.46%, and an average asking direct rental rate reported at $19.16 psf. In June, the Michigan unemployment rate was recorded at 4.1%, a decrease of 0.5 percentage points compared to this time last year. In August, U.S. job openings declined to 10.1 million, the lowest since June 2021, while adding 528,000 jobs, more than double economist’s original estimates of 258,000 jobs. In September, the hiring pace slightly declined due to higher rates and slower company growth with 263,000 jobs added and an unemployment rate of 3.5%, a decrease of 1.3 percentage points compared to one year ago. Year to date the Federal Reserve has increased the interest rate five times. The Federal Reserve has announced they will continue to aggressively institute rate increases until inflation declines and are confident that balance among the economy is being restored. Wall Street closed out the month of September down 9.3%, the worst month since March of 2020. Interest rate hikes have taken a toll on the housing market as home prices have decreased at an accelerated rate, long-term mortgage rates increased for 6 straight weeks by the end of September, and a 30-year rate was recorded at 6.7%, the highest in 15 years. Consumers, employers and the overall market remain aware and cautious heading into the fourth quarter as anticipation builds as the year is ready to close out.

A confluence of events has led Denver to become one of the hottest industrial markets in the country. Robust demand in this regional market with a strong local economy is stemming from the growth of retail sales, employment, and industrial production in the metro area and the greater Colorado region.

The retail market in Portland did not experience much change during the second quarter. With the vacancy rate at 3.2%, net absorption was a positive 83,327 square feet and vacant sublease space increased by 29,737 square feet. There was a slight increase in quoted rental rates, ending at $17.35 per square foot per year. Seven buildings were delivered to the market and 1,129,274 square feet are still under construction.

The second quarter in the Portland Office market ended with a 6.6% vacancy rate. While net absorption totaled a positive 1,160,537 square feet, vacant sublease space increased to 334,810 square feet. The quarter finished with rental rates at $23.81, which remained the same from the first quarter. Five buildings were delivered to the market with 2,503,330 square feet under construction at the end of the quarter.

The second quarter has come to a close with a vacancy rate of 3.7%. Net absorption totaled a positive 713,455 square feet and vacant sublease space increased. Rental rates increased to $8.16 and nine buildings were delivered to the market. Those nine buildings totaled 552,369 square feet and 4,846,902 square feet remain under construction at the end of this quarter.

TCN Worldwide's State of the Market: Western Edition, 3rd Quarter 2017 Prepared by Hugh F. Kelly, PhD, CRE, Consulting Economist to TCN Worldwide. In this edition: –National and Macroeconomic Overview –Regional Economic Conditions –Commercial Property Investment Trends

{kind=link}