Overview of National Economic Context

The major macroeconomic indicators. The U.S. economy had strong momentum as 2015 ended. Recently revised employment data shows that 851,000 jobs were added in the Fourth Quarter, bringing the total to 2.7 million for the year. This allowed the unemployment rate to fall to 5.0%, an improvement of 10 basis points since September as the rate of new hires tracked by the Bureau of Labor Statistics rose at a 3.6% rate. Inflation for the year was near zero, a mixed blessing: good for consumers, but not so good for retailers; and downright bad for the oil and gas producing regions of the country, which now see crude prices down to $30 per barrel or below. Financial markets started the year in bearish humor, reacting to news of a slowdown in China and fears that Iran’s return to the energy markets will exacerbate the already severe oil glut.

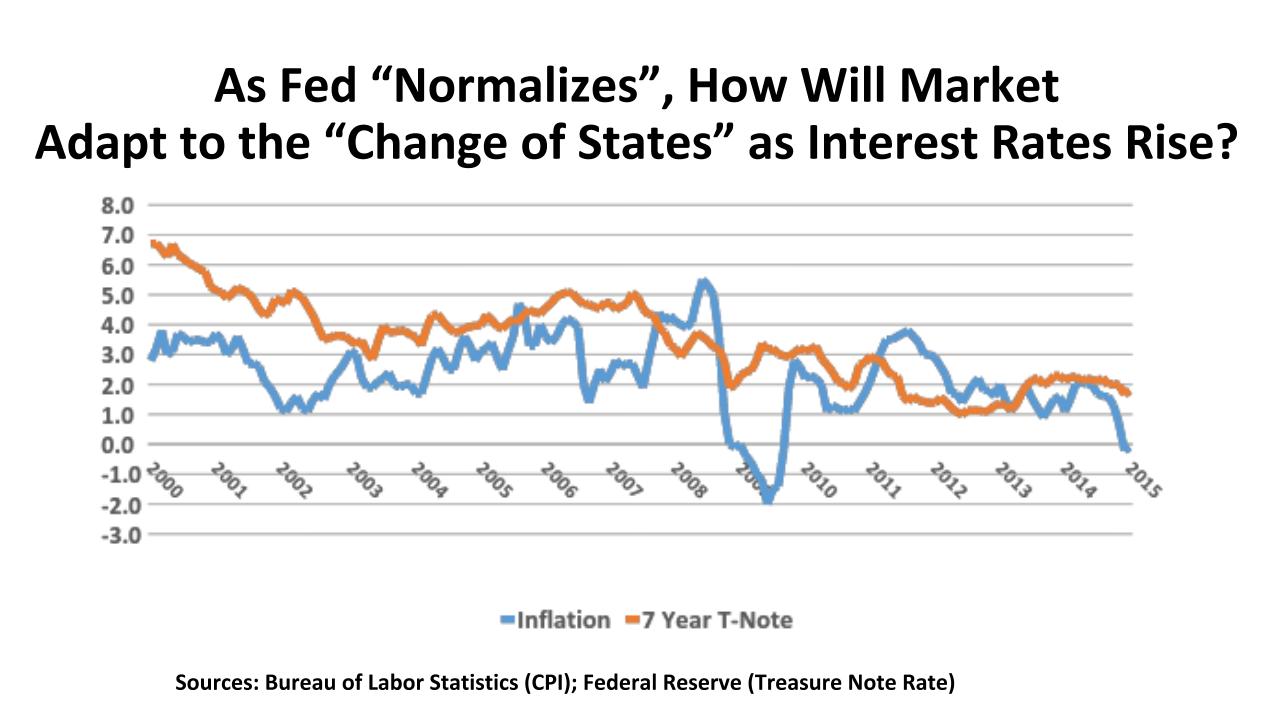

The major policy indicators. The long-anticipated “normalization” program for the Federal Reserve was initiated by a modest 25 basis point increase in short-term rates by the Board of Governors. The plan is to move rates upward with great caution, depending upon economic trends. A five-year, $305 billion Transportation bill was passed and signed into law with just hours to spare in early December, providing funds for both highway and transit programs. However, with just 115 laws passed in 2015, the 114th Congress is on track to be one of the least productive in history. Fiscal policy has been hostage to gridlock in Washington throughout this current decade. In a presidential election year, it is unlikely that any meaningful new initiatives will alter Federal policy in 2016.

The Outlook. Forecasters are increasingly jittery about American economic growth in 2016. The Blue Chip Economic Indicators panel held its prediction for real GDP increase to 2.5% in both 2016 and 2017, but the fifty economists comprising the panel express concerns about the impact of a strong dollar on U.S. export, worries about an international slowed in China and other emerging markets, and the overhang of excess supply of petroleum in the world markets. Interest rate increases should be expected, but not disruptive to growth. If oil prices have bottomed out, a small (and somewhat welcome) uptick in CPI inflation can be expected. On a positive note, the forecasted jobless rate is anticipated to drop to 4.8% in 2016, and 4.6% in 2017, producing some growth in incomes and in consumer spending.

Regional Conditions in the Central States

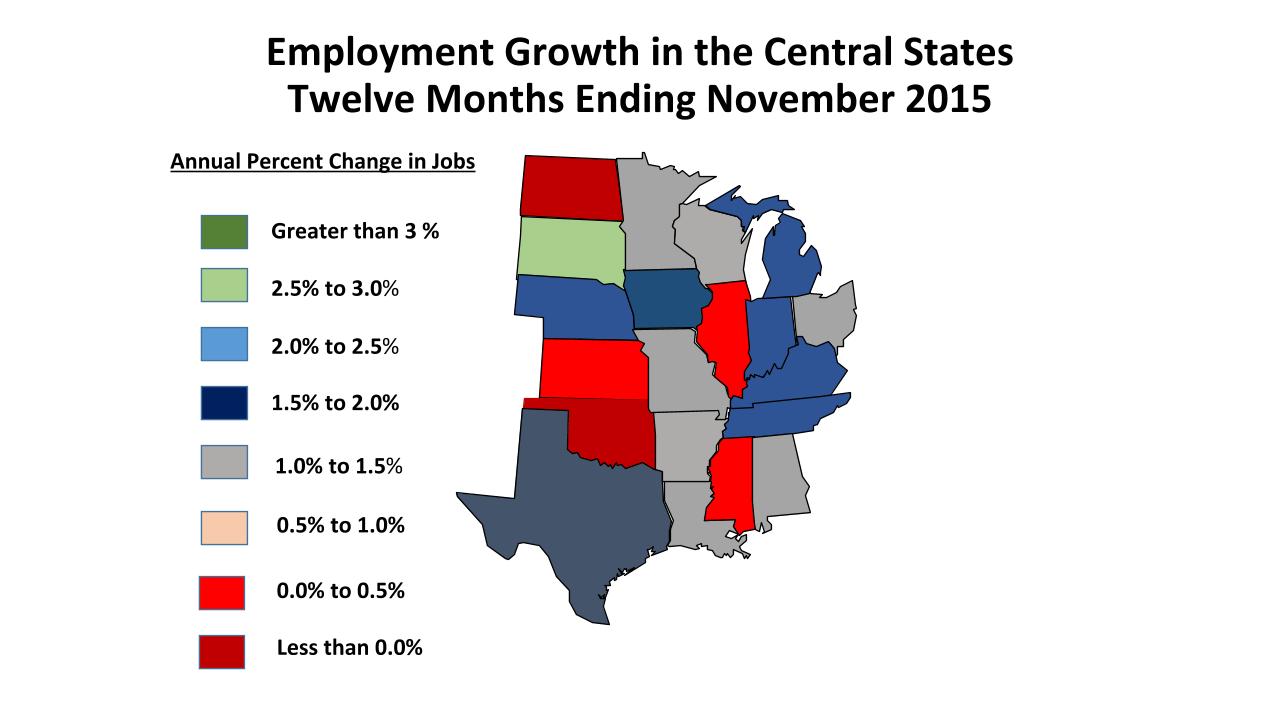

Employment Trends. After a solid run of enviable job growth, the Central states have hit a stumbling block – and not for the first time. This resource-rich region could boast of leading the nation into an era of energy independence. But its own dependence upon “black gold” and related products is now a handicap as the price of West Texas Intermediate Crude has fallen from about $103 per barrel in July 2014 to its January 19, 2016 spot price of $28.47. So the employment boom that extended from Texas’ Permian Basin to the Williston Gas Fields in North Dakota has come to a crashing end, for now.

Texas still has enough economic strength to post a job gain of 179,300 in 2015, third in nation behind California and Florida, and just ahead of New York. But for Texas the 1.5% growth rate those jobs represent don’t count for its accustomed bragging rights. Compared to the balance of the South Central region, though, Texas is in pretty good shape. Louisiana and Oklahoma ended the year in negative territory. Kansas’ job gain was just 7,000 (0.5%) and Arkansas saw a net job gain of 14,700 (1.2%). North Dakota, however, was the hardest hit as its Bakken oil boom went bust, costing the state 13,500 jobs (-2.9%) last year.

Against this background, the so-call Rust Belt is looking pretty good. Ohio and Michigan are both up more than 70,000 jobs year-over-year, for growth rates of 1.4% and 1.7% respectively. Indiana’s employment grew by 58,500, a 2.0% gain that compares favorably to the national total. Interestingly, while automotive production is edging ahead, metals manufacturing targeted for the aerospace industry is credited with providing much of the forward momentum.

Macro-economic conditions. Import/export activity is associated with coastal locations in the popular mind, but the Central states are incredibly connected to the global economy. That has been a mixed blessing in recent months. Agriculture is one of America’s few sectors with a consistently positive trade balance, but the combination of the strong dollar and good harvests have kept profits in the farm sector constrained. Energy, as previously noted, has turn from an accelerator to a drag for the region. There are major equipment manufacturers, such as Caterpillar and John Deere, whose production is tied to the export markets and for whom the slowdown in China is a material factor.

On the positive side, several years of excellent growth have bolstered both household incomes and balance sheets, and so the Central states have some resilience, especially if the general U.S. economy remains strong. States from Nebraska and Minnesota into the Mid-South area of Kentucky and Tennessee are seeing a more important role for the service sector as well. Nashville is building a renewed reputation as an 18-hour city, and Minneapolis-St. Paul is enjoying strong growth in the medical and education sectors, building on a solid base in the STEM (science, technology, engineering, and math) disciplines.

Commercial Property Investment Trends

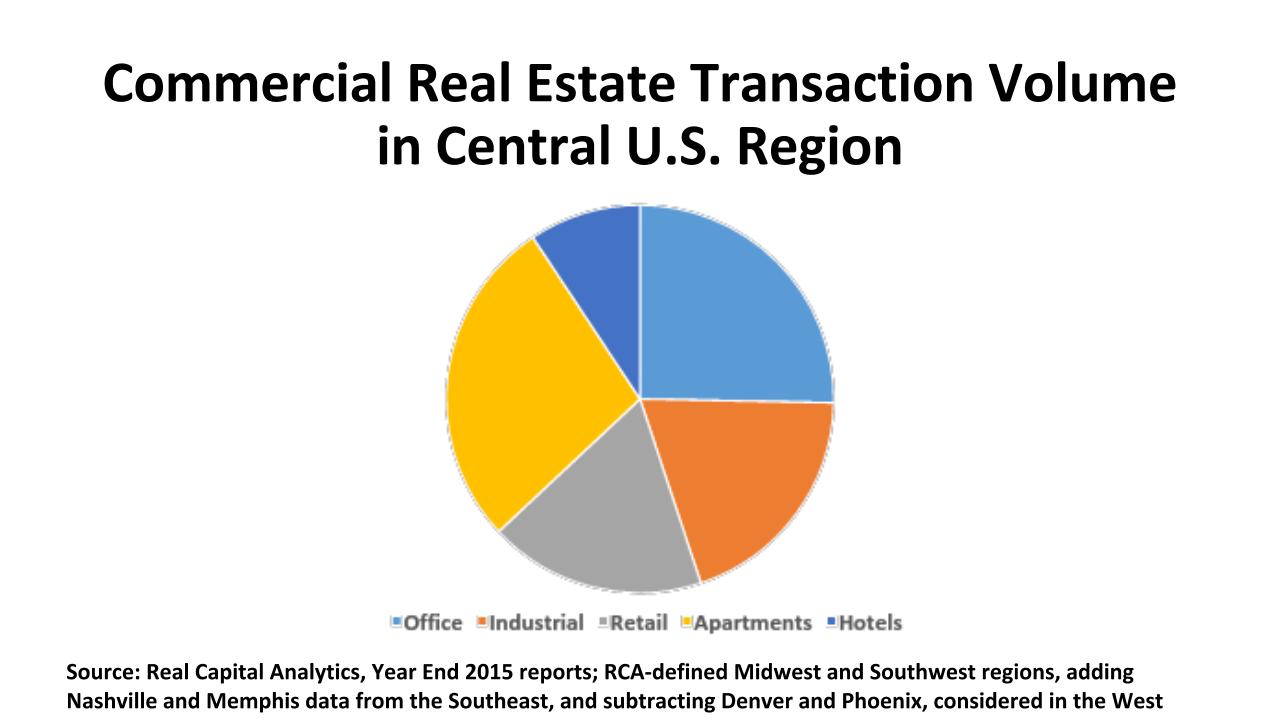

Office. With $8.7 billion in office building sales transactions in 2015, Chicago trailed only Manhattan in investment volume. Three-quarters of that volume was in the CBD – led by Blackstone’s $1.3 billion acquisition of the Willis Tower. In the aggregate, the Central states accounted for $34.4 billion in office deals during 2015 – and more than 65% of the dollar volume was directed to suburban properties. In this, the region differs from the rest of the U.S., where about half the dollar volume was registered in downtown properties. The leading suburban office markets in the Central states were Dallas ($3.4 billion), Houston ($2.4 billion), Chicago ($1.9 billion), and Minneapolis ($1.0 billion).

Emerging Trends in Real Estate surveys nearly 1,500 real estate professionals for its annual publication. One of the questions asks for “Buy/Hold/Sell” recommendations by market and by property type. Four Central states metro areas were listed on the Top 20 “Buy” list for offices, led by Minneapolis- St. Paul, ranked second in the nation. Also listed were Nashville (#7), Dallas-Ft. Worth (#10), and Chicago (#17).

Industrial. With just of $21 billion in warehouse/distribute and flex space sales in 2015, the Central states accounted for 27.5% of the nation’s $76.5 billion in industrial property transactions. Chicago, one of the nation’s largest concentrations of warehousing (more than a billion square feet of space), unsurprisingly saw the greatest concentration of industrial investment, just over $4 billion in 439 individual properties. Houston, Indianapolis, Memphis, and Austin all tallied between $1 billion and $2 billion in industrial property transactions last year.

The Central states also garnered enthusiastic support in Emerging Trends’ “Buy/Hold/Sell” rankings for industrials in 2016. Chicago (#2), Minneapolis (#4), and Indianapolis (#5) were right in the first tier of the Top 20. They were joined by Dallas-Ft. Worth (#7), surprising St. Louis (#9) and Detroit (#10), and Nashville (#16). If the industrial sector represents the “back to basics” choice for investors, with solid demand from traditional sources augmented by e-commerce fulfillment activity, it appears that the Central states are capturing a significant share of the benefit.

Retail. Shopping center and other retail property sales in the Central states totaled $20.4 billion in 2015, about evenly divided between strip centers (neighborhood and community retailing) and malls/power centers and specialty retail. That is a different distribution from the balance of the country, where neighborhood/community centers accounted for just 41% of retail property investment volume. This is consistent, however, with the region’s suburban weighting in the office sector. By and large, the Central states are not home to the 24-hour city markets (Chicago being the exception), nor to the 18-hour city configuration (again, excepting Nashville and Austin).

Perhaps, then, there is a lesson in the Emerging Trends’ “Buy/Hold/Sell” rankings for retail assets in 2016, because it is only Austin (#3) and Nashville (#7) that earned Top 20 rankings from the respondents to that survey. Emerging Trends identifies Austin as a market where growth in population is buoying demand for new retail development. And, like Austin, Nashville is lauded as a market where both downtown vibrancy and attractive suburban locations combine to provide great choices for consumers, whether local residents or visitors to these “destination markets.”