Overview of National Economic Context

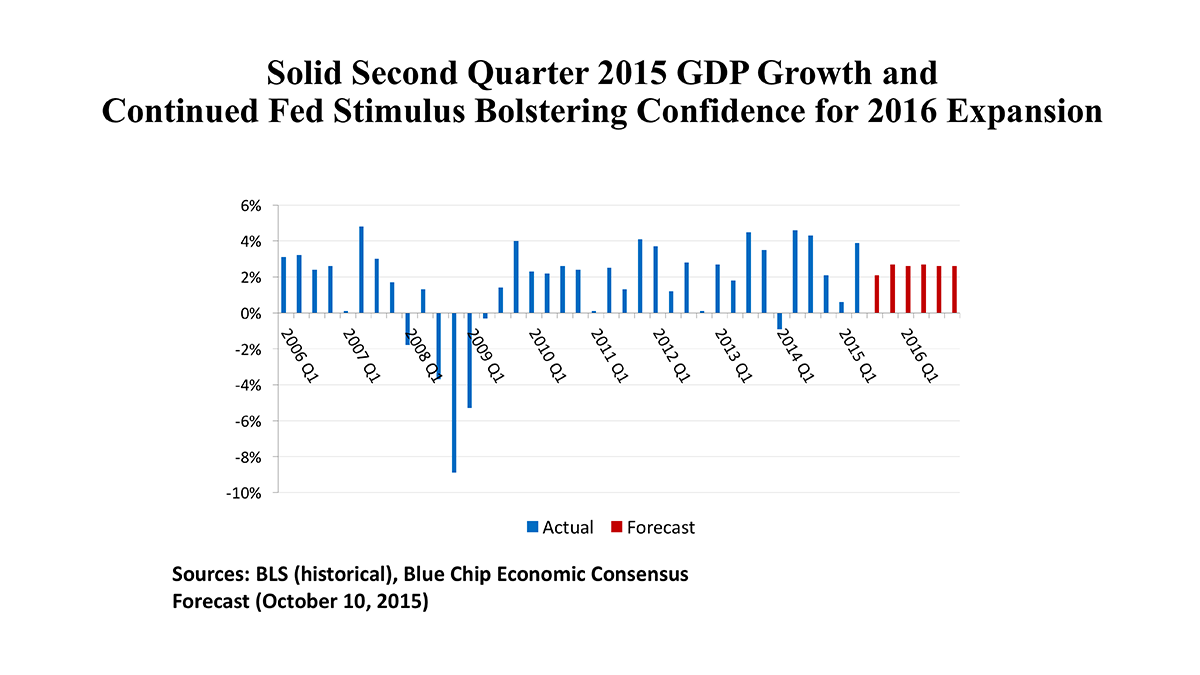

The major macroeconomic indicators. After a slow first quarter (again attributed to a severe winter), the economy picked up the pace and the most recent GDP estimate registered 3.9% growth. Employment has been increasing at 2.9 million jobs at an annual rate, or 2.1%, bringing the headline jobless rate down to 5.1% as of September. Low energy prices have driven the CPI down to 0.2%, year-over-year, and core inflation (excluding food and energy) is muted at 1.8%. The housing recovery is seeing existing home sales at 5.3 million unit pace (up 6.2% from a year ago), with prices 4.7% over a twelve-month span. Thus far in 2015, retail sales have been tracking job growth nicely, with a 2.1% increase annual increase as of August 2015.

The major policy indicators. Federal Reserve policy remains pro-growth, as the September meeting held interest rates near the zero bound. Banking regulators are walking a delicate line between safety (seeking to avoid a repeat of the 2007 – 2009 financial crisis) and liquidity (using the low Fed borrowing rate to encourage banks to earn spreads by increasing loan activity). Real estate has been able to access debt funding across a range of lenders. Fiscal policy remains captive to Congressional gridlock, though. Exporters are being hobbled by the de-funding of the Export-Import Bank, and badly needed infrastructure work is stalled as the Transportation Bill has been bottled up. As far as progress is concerned, Washington continues to try to row with one oar out of the water.

The Outlook. The Blue Chip Consensus forecast is calling for 2.7% GDP growth in 2016, accompanied by tighter labor markets (a 4.7 unemployment rate by the end of next year), and modestly higher inflation (a CPI increast of 2.7%). Interest rates will still be very low by historical standards, with a 1.4% 3-month Treasury rate, and 3.2% for the yield on the 10-year Treasury. Personal income is forecast to rise by 2.6%, and with increased consumer confidence, personal expenditures are predicted to advance by 2.9%. Housing starts are expected to rise to 1.3 million homes, as a solid economy supports a further residential rebound.

Regional Conditions in the Central States

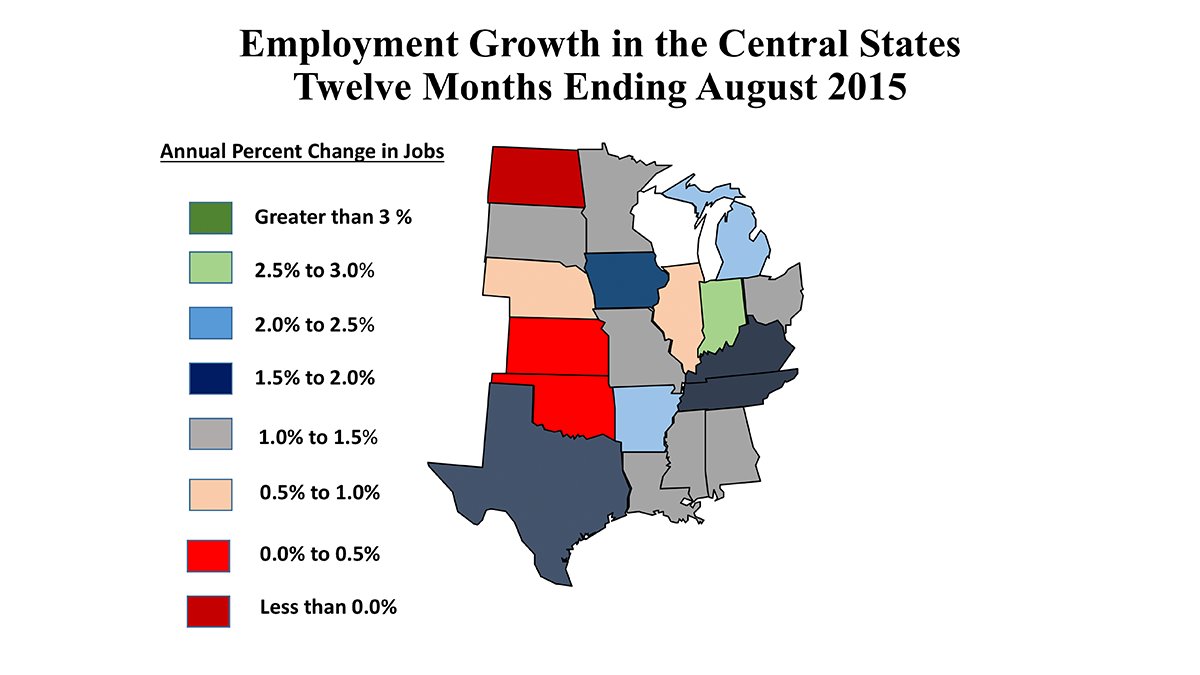

Employment Trends. Reports that “modest” job increases reflect labor market conditions in the Central states fall into the “glass half-full” category. Of the 19 states between the Appalachian and Rocky Mountains, only three (Indiana, Michigan, and Arkansas) exceeded the nation’s employment growth average for the 12 months ending August 2015.Indiana enjoyed across-the-board gains, led by increases in manufacturing and trucking, bolstered by hiring in healthcare and in government as well. In all, the state added 76,000 jobs, or a 2.5% increase.

Michigan led in absolute job increase, 91,000 jobs (2.2%). Resurgence in the automobile sector, the state’s basic industry was the catalyst, but gains in white collar jobs contributes as well, with professional and business services, education and healthcare solidly in the plus column. In Michigan, all gains were in the private sector as government employment dropped by 8,000 jobs. Arkansas added 27,000 jobs (2.3%), mostly in white-collar sectors like finance, business services, education and health.

For the rest of the region, both energy and agriculture presented headwinds to the job market. The boomtowns of North Dakota’s exploration and drilling surge are seeing an outflow of population and jobs in the wake of the energy price collapse. Texas’s growth rate ratcheted back to just 1.9%, although this still represented a net gain of 218,000 jobs for the state. Seven of the 19 states are coded in gray on the map, indicating a growth rate of between 1.0% and 1.5%, slogging ahead, but hardly seeing a robust trend as we turn toward the end of 2015 and into 2016.

Factors Affecting the Region. When the Producer Price Index for energy products drops 15% during the course of a year, that’s good news for drivers at the gas pumps, but it spells trouble in the oil-and-gas producing states of the Central U.S. At the same time, the Federal Reserve’s Beige Book summary of current economic conditions reports instances of declining agricultural prices, weakening farm credit conditions, and areas of drought and/or severe storms affecting the Breadbasket states. While the situation is hardly dire, the Central region has rotated away from being an economic engine for the nation – as it was for several years recently – into a more reactive condition. With US GDP forecast to grow by 2.7% in 2016 and further declines in unemployment, the Central states may have touched a cyclical bottom in 2015 and may see the stronger regional economies on the Coasts as growing markets for the goods and services produced in America’s heartland.

Commercial Property Investment Trends

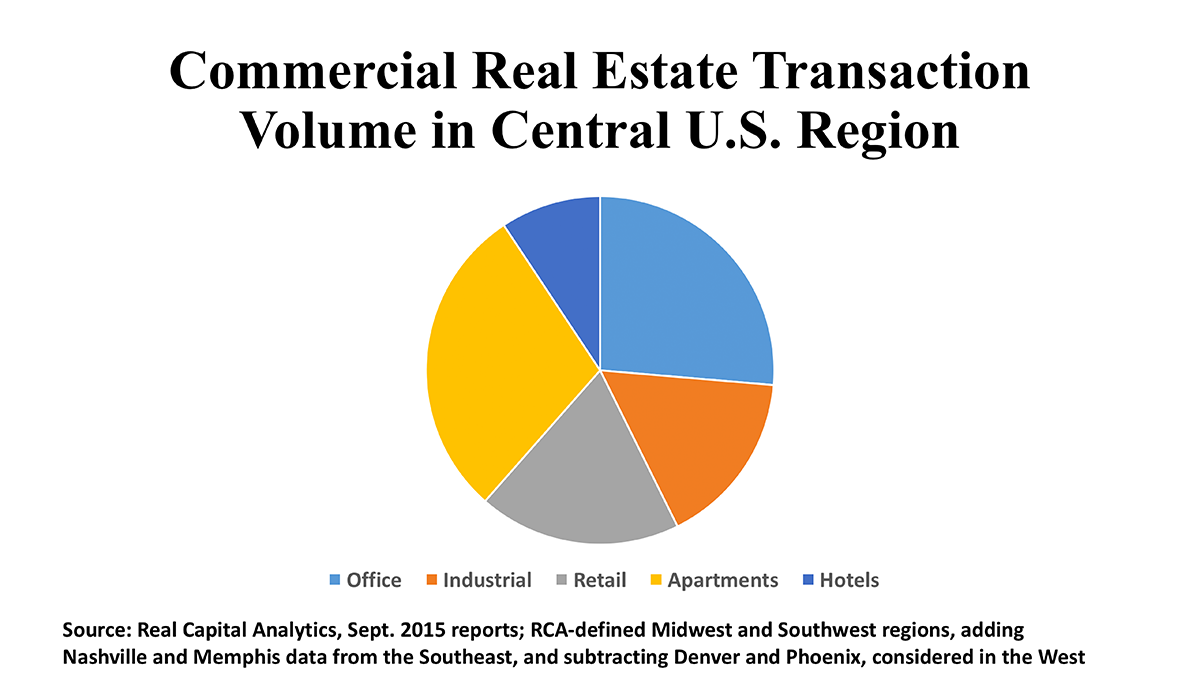

Offices. Investment in the Central States office markets has been moderately active thus far in 2015, with aggregate purchases of $18.9 billion tallied from just over one thousand transactions. Prices per square foot are running below the U.S. average, except in the Texas cities of Austin and Houston, and cap rates tend to be higher than elsewhere in the country – reflecting higher initial yields, but also a higher risk premium due to the volatility in local markets here.

In most Central office markets, it is private rather than institutional investors that dominate the purchase patterns. International investors have targeted Houston of late, accounting for about a quarter of the 2015 purchases in that city. They have been joined by REITs, who have been the buyers in 23% of Houston’s deals. That’s the exception, though. Dallas finds private buyers accounting for 46% of its office transactions, and in Austin the figure is a staggering 63%. Similarly, the Ohio cities of Columbus, Cleveland, and Cincinnati draw largely on private investors for their office deals.

The pattern changes somewhat in a few places. Chicago finds large equity funds claiming 44% of its office transactions, followed by institutional investors at 22%. This is a key market, as the largest city in the Central states and also the principal target for office investors, with $6 billion spent in 136 transaction so far in 2015. Minneapolis accounts for nearly half of its office deals from institutions (24%) and equity funds (25%), though private purchases exceed both with a 31% share.

Industrials. At $11.9 billion in aggregate industrial investment so far in 2015, the Central states lag the West ($17.5 billion) and the East ($15.0 billion) in a property type that should be exceptionally strong due to locality and due to economic base. Volatility is the key issue constraining investment capital flows, and this is apparent in the high risk premium that has kept industrial cap rates above 7.5% on average in the Central Region. The U.S. average industrial cap rate is 6.9%.

That’s the challenge. But the good news is that international investors are stepping up to meet the challenge. A full 31% of all industrial property purchases in the heartland states have sourced cross-border capital. That share rises to 57% in Chicago, 52% in Austin, 44% in Memphis, and 39% in Dallas. And, in San Antonio, it is a breath-taking 67%, although San Antonio’s sample size is a small 37 transactions for 2015. Perhaps the international buyers are seeing greater long-term potential than domestic investors at this point.

Only Chicago has stepped over the $2 billion threshold in industrial sales this year, with Dallas second in the region at $1.7 billion, and Houston third at $1.1 billion. Even these cities, though, are punching below their weight, given the enormous seize of their industrial property inventories.

Retail. There have been 1,370 shopping property deals recorded in the Central state in 2015, generating $13.5 billion in aggregate sale price. Thus, proportionately, retail investment activity mirrors what we have discussed above in the office and industrial sectors. Investors as a a group have been responding to a perception of slower regional economic growth. Nationally, retail property has been transacting at an average price of $226 per square foot. Of the markets in the Central region, only Chicago ($236) and Dallas ($241) surpass this benchmark. Likewise, the mean U.S. retail cap rate is 6.5%, but the Central states have a nearly 7.0% average cap rate, with only Chicago (6.5%), Austin (6.1%), and St. Louis (5.8%) displaying cap rates stronger than the national norm.

The higher cap rates may reflect the cross-section of buyers. Here, as in the office and industrial property types, it is private purchasers, often with higher yield requirements, that have the largest share of the acquisition market. REITs have a significant position in the retail property sector, but many markets in the Central region have attracted little interest from the trusts. The exceptions are Austin, Columbus (Ohio), and Minneapolis. By and large, few institutional investors such as pension funds and life companies have appeared on the buy side for retail properties here. In the absence of such large national and international players, local savvy investors may see an opportunity to acquire good operating assets at attractive prices.