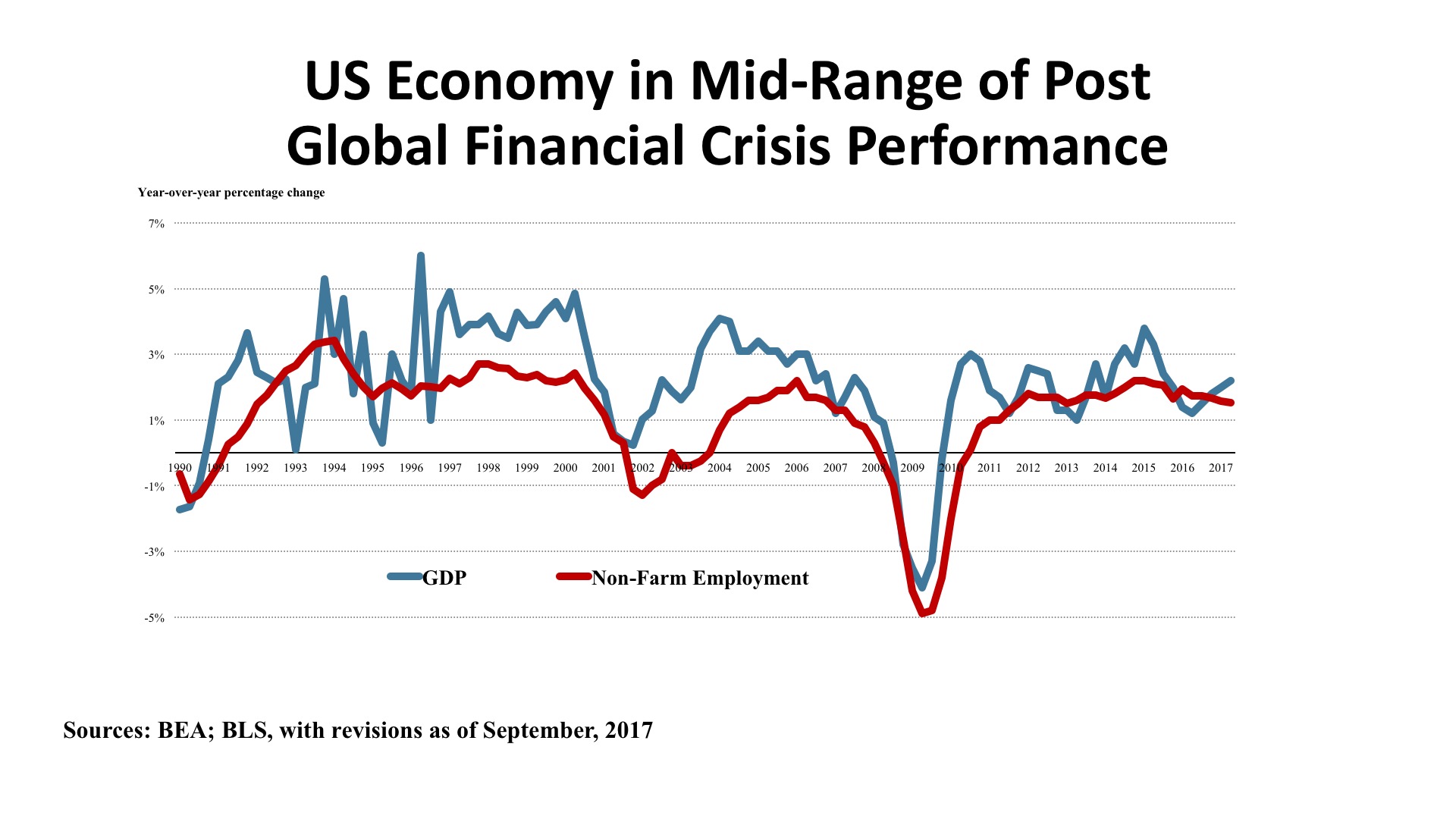

Mixed Signals Typify the Reports from Key Economic Sectors.

Natural catastrophes, including a devastating series of hurricanes and an intense wildfire season in the Western United States, have stressed many regions of the country during the third quarter of 2017. Nevertheless, the economy has thus far held steady within the moderate bounds of growth that have typified the recovery from the Global Financial Crisis of a decade ago. Although short-term impacts of the storms and fires will make headlines, the economy is large and resilient. It should sustain momentum with year-over-year GDP growth of 2.0% - 2.5% for both the remainder of 2017 and through 2018.

Mixed signals typify the reports from key economic sectors. Consumption, which represents about 70 percent of the U.S. economy, had a second-quarter uptick as it did a year ago. In 2016, second quarter personal consumption grew at an annualized rate of 3.8 percent (up from 1.8 percent in the first quarter). This year, second quarter spending hit 3.3 percent (up from first quarter’s 1.9 percent). This pattern of a weak first quarter has frequently been seen since 2010. Existing home sales are running at 5.35 million, up just 0.2% year over year, the median home price is up 5.6 percent from a year ago. An increasing trade deficit acts as a depressant on GDP growth, and while real exports have been up 1.9% (as of August), real imports expanded more quickly at 2.8 percent.

Jobs. Nate Silver’s popular book on interpreting statistical data, The Signal and the Noise, cautions against the tendency to take one or two bits of information and extrapolating them into a presumed “trend.” So we shouldn’t make too much of the September employment report that tallied a 33,000 job loss, the first after 83 consecutive months of gains. Hurricanes Harvey and Irma impacted the market as the Bureau of Labor Statistics were collecting the September numbers, and when the October figures for U.S. Caribbean territories come in there will be an added effect measured. But recovery efforts will, later on, bolster the job picture. That’s important for the on-the-scene workers, but statistically, it is economic “noise.”

The “signal”, however, should give us deeper concern. That is the true trend, and it is measured by the now two-year-old slowdown in job growth – even before the storm impacts. Employment growth from mid-2014 until October 2015 posted year-over-year gains of two to 2.3 percent. We have not seen two percent growth since then, and average 1.5 percent for the first half of 2017. So the trend is a slow but persistent attenuation of job gains.

As we have indicated before, this is a story of increasing labor shortage caused by age demography, technological change, and a slowdown of new immigrant workers. The BLS “JOLTS” report (Job Openings and Labor Turnover Survey) showed healthcare and social services openings up 71,000, but declines in manufacturing (17,000), education (51,000), and other services (95,000). Overall, through August, the annual new hires tallied 63.8 million workers, versus 61.7 job separations, for a net gain of 2.1 million. This has been enough to drop the official unemployment rate to 4.2 percent, as of September.

Policy. Thus far, deregulation by executive order and by agency implementation has been the principal policy tool put to effective use in the first year of the Trump administration. In this, Federal policy has aligned with Wall Street hopes and expectations, extending the post-election bump well into 2017 and driving the DJIA up to 22,871 as of October 13, 2017 – or 26.4 percent higher than a year prior.

This is in contrast to the difficulties of moving fiscal policy forward by means of legislation, where healthcare reform efforts floundered, tax code changes remain at a nascent stage, and infrastructure investment has been deferred without much comment. Perhaps the President’s comment on healthcare covers the legislative agenda generally: “Who knew it was so complicated?”

As has been the case for a decade now, it is at the Federal Reserve where policy has been most effective and most transparent. Looking at the “signal” rather than the “noise,” the Fed is on a slow but steady course of tightening monetary policy, by moving interest rates gradually upward (despite still languid inflation) and reducing the huge balance sheet of assets acquired during the Quantitative Easing programs. Feeling that the markets are well-served by predictability, the Fed has been clear that its intent is to maintain a path of incremental adjustment rather than drastic policy shifts.

Outlook. There has been little change in outlook since the last edition of the TCN newsletter was prepared in July. GDP growth will fluctuate from quarter to quarter but stay in the 2.0 to 2.5 percent range on a year-over-year basis. Some upward drift in interest rates can be expected, but many are tiring of the wait for higher rates and believe it will be more than a year before the ten-year Treasury yields three percent. For the first time in decades, we may see a “soft landing” to an economic cycle rather than a hard recession. Right now, it looks like geo-political risk rather than economic dislocation is the main threat on the horizon. One variable to watch, though, is the continued widening of the incomes gap, likely to be the factor with the greatest potential to destabilize the trend of moderate upward expansion we have recently enjoyed.

Economist Bio: Hugh Kelly, PhD, CRE

Kelly began teaching at NYU Schack, a division of the NYU School of Continuing and Professional Studies, in 1984. He currently teaches graduate-level courses in “Real Estate Economics & Market Analysis,” “Risk & Portfolio Management,” and “Urban Economic Development.” Kelly specializes in development of economic and market forecasts, portfolio strategy, and seminars and workshops. He heads his own consulting practice, Hugh F. Kelly Real Estate Economics, which serves national and international real estate investment and services firms, governmental organizations, law firms, and not-for-profit agencies. Previously, he was chief economist for Landauer Associates, where he worked for 22 years until early 2001. Kelly also served as the president of the board of directors of the Brooklyn Catholic Charities’ affordable housing development corporation (2006–2012), and is an avid industry spokesman. The author of more than 200 articles in industry journals, Kelly recently published a paper on contemporary politics and economics, “Judgment: Imagination, Creativity, and Delusion,” in the philosophical journal Existenz. He is widely known for his research on 24-hour cities and commercial real estate investment performance. A member of The Counselors of Real Estate since 1989, Kelly has served on many of the organization’s committees, including as editor-in-chief of the group’s esteemed peer-reviewed journal, Real Estate Issues. Kelly earned a Ph.D. at the University of Ulster (U.K.) and a B.A. at Cathedral College (New York).

Kelly began teaching at NYU Schack, a division of the NYU School of Continuing and Professional Studies, in 1984. He currently teaches graduate-level courses in “Real Estate Economics & Market Analysis,” “Risk & Portfolio Management,” and “Urban Economic Development.” Kelly specializes in development of economic and market forecasts, portfolio strategy, and seminars and workshops. He heads his own consulting practice, Hugh F. Kelly Real Estate Economics, which serves national and international real estate investment and services firms, governmental organizations, law firms, and not-for-profit agencies. Previously, he was chief economist for Landauer Associates, where he worked for 22 years until early 2001. Kelly also served as the president of the board of directors of the Brooklyn Catholic Charities’ affordable housing development corporation (2006–2012), and is an avid industry spokesman. The author of more than 200 articles in industry journals, Kelly recently published a paper on contemporary politics and economics, “Judgment: Imagination, Creativity, and Delusion,” in the philosophical journal Existenz. He is widely known for his research on 24-hour cities and commercial real estate investment performance. A member of The Counselors of Real Estate since 1989, Kelly has served on many of the organization’s committees, including as editor-in-chief of the group’s esteemed peer-reviewed journal, Real Estate Issues. Kelly earned a Ph.D. at the University of Ulster (U.K.) and a B.A. at Cathedral College (New York).